What are the three most powerful words in institutional investment?

Hello Fusings Fans,

I’m Jordan, the freshest Fuse Partner. The new onboarding ritual here is to give the rookie the keys to the blog and see how things go. Allow me to briefly introduce myself before we get into it.

We’ll get the chance to know each other over the next few posts, but here are the Coles notes on me. I’ve spent close to 15 years working in, with, and around Canada’s leading financial institutions, often finding myself in roles so new they didn’t have names yet.

I was the person you called if you had a hunch something didn’t make sense, you wanted help understanding it and you needed to craft a strategy and story to do something about it.

Questions like: “What does commercial real estate look like in the face of WeWork?” “How will the Future of Aging shape the Pension mandate?”, “How will changes in society drive changes in infrastructure investment opportunities?” and “How can institutional capital allocators thrive in uncertainty?” (This last question bothered me enough to do a PhD on the topic. More on this later…)

The common theme here is getting comfortable with uncertainty, which is a good place for this series to start.

Over the next few weeks, we’ll explore several topics that keep institutional investors up at night. These topics reflect our clients’ most wicked problems and our spiciest internal debates. We are building towards our concept of Capital Design – blending investment rigor with design logic.

The journey starts here – we welcome your feedback along the way!

“It’s not what we know that gets us into trouble.

It’s the things we know for sure that just ain’t so.”

– Mark Twain

Knowledge, White House Press Conferences, and Elevator Small Talk

Picture this: my second week at Fuse, stuck waiting for an elevator with fellow Fuse partners Hussain and Chaz, when our version of small talk dives into the deep end of knowledge itself. Enter Donald Rumsfeld, circa 2002, dropping his infamous take on uncertainty. His breakdown of knowns and unknowns isn't just Pentagon speak; it’s a critical lens for understanding the nature of risk, certainty, and the dreaded unknown.

The pension funds we work with have the noble yet challenging task of investing today’s dollars to pay tomorrow’s pensions.

Our clients are therefore in the business of navigating risk and uncertainty.

Therefore, it’s a conversation worth amplifying here.

I just called to say “we can’t know”

At Fuse, we believe we can’t properly discuss something unless we can define it. For this, we’ll call in the intellectual heavyweights.

According to renowned Decision Sciences scholar Paul Schoemaker, knowledge exists on three levels: certainty, risk, and uncertainty. “These levels differ in their approach to probability, from not needed (certainty), readily available (risk as in life insurance), and nearly impossible to assess (uncertainty).”

Why does this matter to institutions like pension plans?

Because risk can be quantified, but uncertainty cannot.

However, the institutional investment process sometimes conflates the two. Uncertainties are often treated as risks with low probabilities.

Speaking from experience in the trenches, doubt in the investment process often stems from uncertainties being labeled as risks. “We don’t know” is often viewed as a failure of analysis or work ethic when we’re actually solving the wrong problem altogether.

True uncertainties are things we can’t know. And, while for very good reasons, Institutional investors are deeply uncomfortable saying “we don’t know”—it’s even rarer to hear “we can’t know.”

Why does this happen? Institutional investors are efficient decision-making machines. When given a set of familiar-looking investment opportunities, they excel at thorough diligence toward an investment decision.

The assumption is that gaps in the data can always be filled with more time and resources, and that risk categories are suitable for assigning risk-adjusted return expectations, given assumptions about how the world operates.

However, true uncertainty disrupts this machinery. It hides in plain sight, under the guise of things we think we know.

Is it better to have known and lost, than to have not known at all?

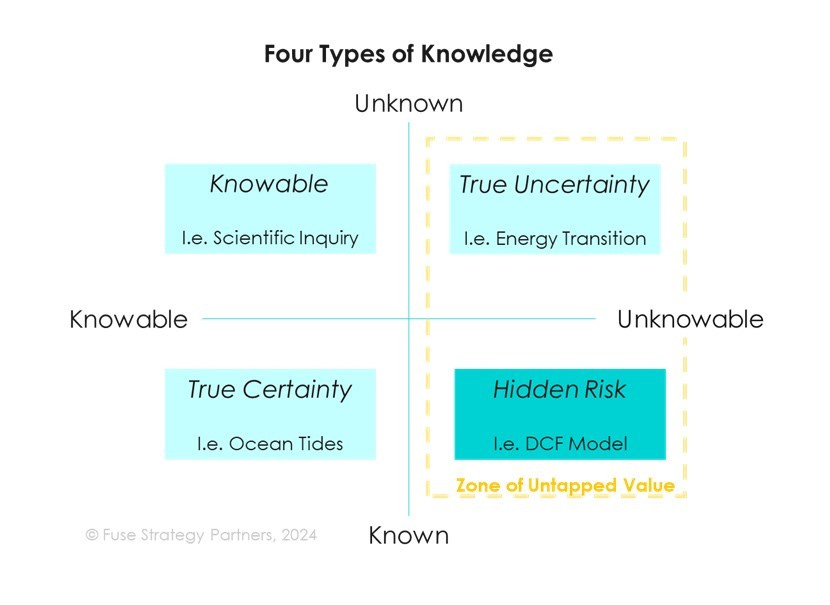

Rumsfeld’s analogy left out a crucial category—one with broad implications for institutional investors: the “unknowable known”—i.e., the things that institutions think they know but are truly unknowable.

For those of you playing consultant bingo, you get to fill in your 2x2 square now. The oft-mocked grid is yet to be bested as a tool for visualizing a complex situation, simply. This one maps the 4 types of knowledge.

Investment professionals should focus on the right-hand side for new sources of value creation.

First are the things we think we know but can’t know, in bottom right quadrant.

Take, for example, the discounted cash flow models that drive private asset valuations. The last cell in a 40-year projection gets as much credibility as the first. The data assumes reversion to historical means, using inputs that can be easily quantified. False certainty here can paper over material risks to the underlying asset. More fiction has been written in Excel than Word, after all.

The second is the things we don’t know and can’t know, in the top right quadrant.

This is the big, messy, changing world “out there.” Let’s use the energy transition as an example. How much of an investment’s value derives from social, technological, economic, ecological, and political factors that don’t fit neatly into an analyst’s model? How does an asset’s on-paper risk profile reflect the true strength of its business, given how much we can’t know about the dynamics that will shape the next 30 years of decarbonization?

This isn’t a philosophical debate anymore. Getting this wrong can mean long-term underperformance.

Starting with “we can’t know” changes what you can know – and do

But there is a way forward. And we believe it begins with the three most powerful words an institutional investor can say: “We can’t know.”

Say it with me. Feels weird at first. But it starts to grow on you.

And if you start with “we can’t know,” you then add “but we can imagine.”

Imagination is the right approach when it’s about creating something new (See Roger Martin on Aristotle’s two modes of thought). We are dealing with “the part of the world where things can be other than they are.” As an institutional investor, you can go a step further and turn something that doesn’t exist yet into something that does.

Thanks to size, scale, and influence, institutional investors are in a unique position to shape unknowns into decisions that benefit them. You can make new markets, entrench new technologies, and shape new channels of value creation for yourselves and others.

Of course, there is lots of stuff we can and do know. But that’s what institutions are already good at. It’s not why you’re reading this. There are lots of good investors and risk managers who can model the knowables with some degree of precision. Those are table stakes.

We believe that investment decisions will increasingly resemble uncertainty rather than risk. And therefore, returns will increasingly accrue to those to those who can best incorporate uncertainty into the investment decision-making process.

The first, best step in benefiting from uncertainty is identifying what we can know but don’t (risks) and what we can’t know but can imagine (uncertainties). Then having a conversation about what we’re really invested in and allocating capital accordingly.

Be humble, make money

Fuse believes that institutional capital will play an even bigger role in transformational investment that drives long-terms returns than it has in the past.

But only if “high conviction investing” cultures can adopt a level of strategic humility. On that vein, we’d love to hear from you at hi@fusestrategy.co:

When is the last time you said I don’t know in an investment context?

What hunches have you had that defy quantification?

What do you know for sure that may not be so?

As this series progresses, I’ll share our approach for helping institutions thrive in uncertainty, by applying new lenses to the capital allocation process. Stay tuned.

| A guest post by

|