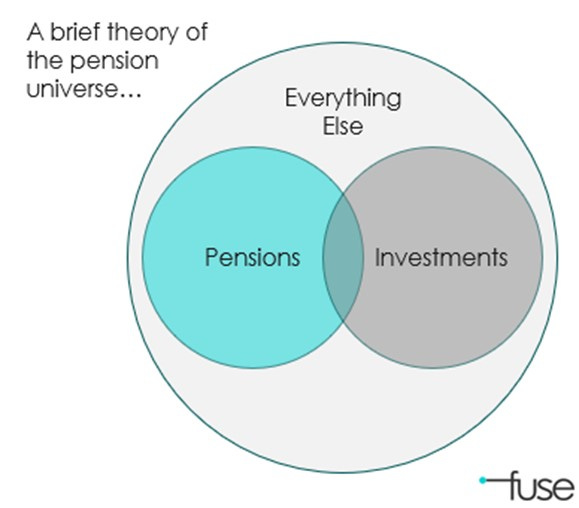

In the beginning, there were pensions.

The modern Canadian pension landscape dates to the 1960s when CPP, CDPQ, HOOPP, and OMERS all came into existence.

And then we said, let there be investments!

The Maple model took shape in the 1990s, when OTPP, OPTrust, CPPIB, BCIMC, and PSP joined the fray and started investing globally, at scale, with in-house managers, and long time horizons.

And all was good. For a time.

The Canadian setup became the benchmark for what world-class governance looked like. More plans emerged, like AIMCo, IMCO, UPP, and others. Interest rates were low, returns were strong, and pensions were paid.

But there was trouble in paradise.

The world kept changing, as it always had. Pension plans were able to keep up for a time by focusing on the central fiduciary responsibilities of pensions and investments. Soon the stuff going on ‘out there’ changed how, and in what ways, we could think about things ‘in here.’

So we looked for new knowledge.

And this is how we arrived at our brief theory of the pension universe today. We have pensions, investments, and everything else.

As we prepare to wrap up 2024, we took a beat to reflect on not just what’s happening around us, but how we can think differently about it. If there’s one thing we have learned from rewarding conversations with Boards, leadership teams, and managers across the country, it is that it is far better to ask the right question than to have the right answer to the wrong one.

We start exploratory strategy conversations by asking “what are you solving for?” We set the boundaries of this question using the constraints set by external forces, according to our brief theory of the pension universe – pensions, investments and everything else.

A few things are changing, driven by external forces.

Pensions are experiencing the impacts of structural forces.

Plan maturity means a smaller ratio of contributors to pensioners puts increased pressure on investment returns to make up the shortfall.

Longer life expectancy leads to a larger liability stream, increasing funding pressures.

The changing nature of work and AI leads to uncertainty around roles, employment status, and career paths.

Changing member expectations push plans outside their historic comfort zones and into new competitive marketplaces.

Investments are subject to growing and new market forces.

The rapid evolution of private asset classes means internal risk and investment processes are less able to accurately underwrite investments and more likely to miss material risks.

Increasing competition and specialization mean you can no longer win with the biggest cheque alone when facing competition from new entrants, megafunds, and strategic investors with different metrics for success.

Scrutiny on costs is mounting. The investment model of Canadian plans has been to hire the best talent and pay accordingly, but there is a greater microscope on this now.

Government intervention is also increasing pressure on plans to invest more domestically, challenging the historic independence of Canadian plans.

So far, so frightening, right? But there’s more!

We see challenges emerging from the overlap between these two domains.

This is especially true for large funds that manage both the assets and the liabilities, but it is also relevant for organizations that manage one or the other. Members care more than ever about the impact their investments have on the world around them. And investment decisions increasingly impact members in some direct or indirect way, especially with unionized populations.

Now for the fun part. That little thing we call EVERYTHING ELSE.

As pensions have grown in membership and assets under management, the “everything else” category is an increasingly big driver of changes for pensions and investments.

What are these forces like? We call them “systemic” because they result from a bunch of individual things interacting with one another, leading to unpredictable outcomes.

Increasing financialization means that as more parts of the economy become investable, previously insulated parts of the economy are exposed to financial risk from seemingly random and uncorrelated sources.

Universal ownership concentrates mega-assets in the hands of a few large funds, which often cross-own parts of multiple assets, exposing all parties to the risk of one.

Risk factors are more interconnected. External factors like pandemics and wars mean multiple parts of the globe and economy are now correlated.

All of this is happening at a time when trust in public institutions is at an all-time low.

We’re pension nerds, so we find this all super interesting. So do lots of other people. But are not telling our clients what to think, but we are sharing frameworks for how to think.

So how do innovative and thoughtful leaders (which, if you are reading this, consider yourself part of the club) think about their roles in the context of the forces that shape our decisions?

How does one think about your contribution to social infrastructure, a vital part of the community fabric for members and their families?

How about your contribution to physical and economic infrastructure, in the assets you manage and the value you create?

And dare we suggest how one might contemplate the political infrastructure that plans play a role in—the often-uncomfortable conversations about inequality, climate change, and civic cohesion?

How many rhetorical questions can a leader tolerate before wanting to see the damn answers?

Consider the triangle.

The traditional triangle from the 1960s is something like benefits, contributions, returns. Or risks, returns, and liquidity, if you’re an actuary.

Given how important pensions are to society, we think about risks, returns, and responsibility. Broadening the last category allows us to think differently about the options available to us as pension leaders.

Innovative pension plans are evolving their understanding of risks, returns, and responsibilities in a complex and uncertain world.

Risk discussions become super interesting in this context. Risks are not individual things anymore but are all connected. They are shifting from focusing solely on the risk of doing to considering the risk of inaction. We are starting to understand how not doing something can be a dicey proposition (even dicier if you don’t realize you’re not doing it!).

Similarly, plans are shifting from individual asset classes to the total portfolio approach. This is a huge cultural shift for plans that have historically given lots of autonomy to their asset classes. Never mind contemplating what comes after the total portfolio approach?

Lastly, we’re seeing plans rethink retirement responsibilities moving away from a simple paycheque to a holistic view of this stage of life. Moving toward behaviourally-informed member segments and away from product-convenient demographics is an excellent way to flip orthodoxies and build better relationships with members.

Furthermore, investment teams can be more open to working with the pension side of the business to solve some of these big challenges with creative new asset classes. In Australia, Aware Super provides an example of this, owning Oak Tree retirement homes, which currently houses more than 1,900 residents and has a portfolio of 48 villages with around 2,550 independent living units.

A constellation of conclusions

What does this all mean for our intrepid readers?

First, everything is connected.

Second, what happens out there matters for what we do in here.

Third, we have the ability and responsibility to stay connected in a complex world.

It’s this last point that I can’t stress enough. We are entering the realm of multi-scale, multi-generational challenges. Yet there’s no one better placed than our Canadian plans to lead the way.

We’ll succeed by staying connected to our members, our stakeholders, and each other. We’ll also have to find new ways to build connections to things that weren’t in our purview but, as we can see now, will be material drivers of our success.

Staying connected is how we think outside the triangle. The world has changed a lot since the 1960s, 1990s, or, heck, even last week!

We’re here for understanding what the next sources of risk, return, and responsibility will be. We hope you’re along for the ride! Let us know at hi@fusestrategy.co.

| A guest post by

|